1060

National Debt

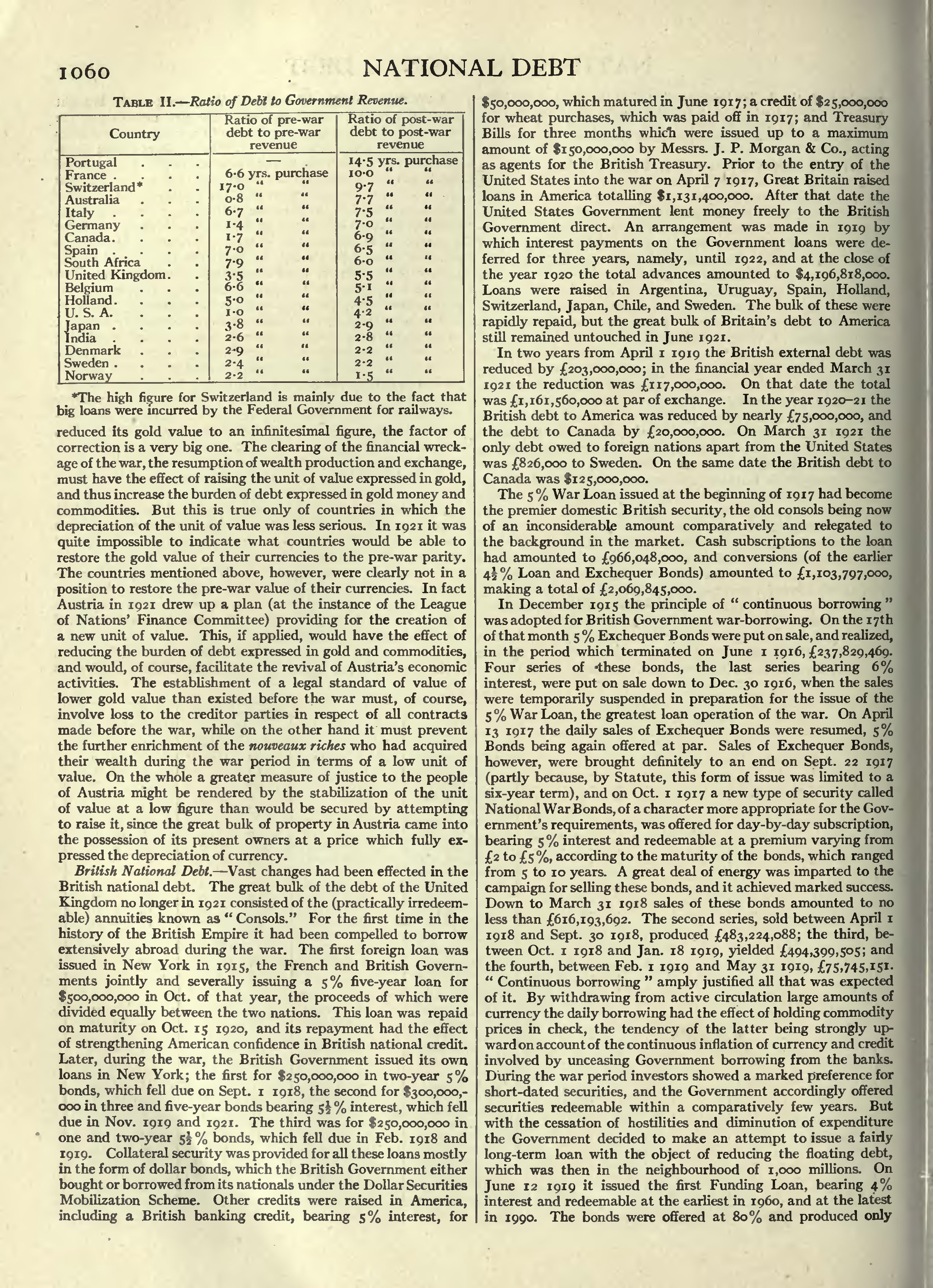

| Country | Ratio of pre-war debt to pre-war revenue | Ratio of post-war debt to post-war revenue |

|---|---|---|

| Portugal | – | 14.5 yrs. purchase |

| France | 6.6 yrs. purchase | 10.0 |

| Switzerland[1] | 17.0 | 9.7 |

| Australia | 0.8 | 7.7 |

| Italy | 6.7 | 7.5 |

| Germany | 1.4 | 7.0 |

| Canada | 1.7 | 6.9 |

| Spain | 7.0 | 6.5 |

| South Africa | 7.9 | 6.0 |

| United Kingdom | 3.5 | 5.5 |

| Belgium | 6.6 | 5.1 |

| Holland | 5.0 | 4.5 |

| U.S.A. | 1.0 | 4.2 |

| Japan | 3.8 | 2.9 |

| India | 2.6 | 2.8 |

| Denmark | 2.9 | 2.2 |

| Sweden | 2.4 | 2.2 |

| Norway | 2.2 | 1.5 |

reduced its gold value to an infinitesimal figure, the factor of correction is a very big one. The clearing of the financial wreckage of the war, the resumption of wealth production and exchange, must have the effect of raising the unit of value expressed in gold, and thus increase the burden of debt expressed in gold money and commodities. But this is true only of countries in which the depreciation of the unit of value was less serious. In 1921 it was quite impossible to indicate what countries would be able to restore the gold value of their currencies to the pre-war parity. The countries mentioned above, however, were clearly not in a position to restore the pre-war value of their currencies. In fact Austria in 1921 drew up a plan (at the instance of the League of Nations’ Finance Committee) providing for the creation of a new unit of value. This, if applied, would have the effect of reducing the burden of debt expressed in gold and commodities, and would, of course, facilitate the revival of Austria's economic activities. The establishment of a legal standard of value of lower gold value than existed before the war must, of course, involve loss to the creditor parties in respect of all contracts made before the war, while on the other hand it must prevent the further enrichment of the nouveaux riches who had acquired their wealth during the war period in terms of a low unit of value. On the whole a greater measure of justice to the people of Austria might be rendered by the stabilization of the unit of value at a low figure than would be secured by attempting to raise it, since the great bulk of property in Austria came into the possession of its present owners at a price which fully ex- pressed the depreciation of currency.

British National Debt. Vast changes had been effected in the British national debt. The great bulk of the debt of the United Kingdom no longer in 1921 consisted of the (practically irredeemable) annuities known as “Consols.” For the first time in the history of the British Empire it had been compelled to borrow extensively abroad during the war. The first foreign loan was issued in New York in 1915, the French and British Governments jointly and severally issuing a 5% five-year loan for $500,000,000 in Oct. of that year, the proceeds of which were divided equally between the two nations. This loan was repaid on maturity on Oct. 15 1920, and its repayment had the effect of strengthening American confidence in British national credit. Later, during the war, the British Government issued its own loans in New York; the first for $250,000,000 in two-year 5% bonds, which fell due on Sept. 1 1918, the second for $300,000,000 in three and five-year bonds bearing 512% interest, which fell due in Nov. 1919 and 1921. The third was for $250,000,000 in one and two-year 512% bonds, which fell due in Feb. 1918 and 1919. Collateral security was provided for all these loans mostly in the form of dollar bonds, which the British Government either bought or borrowed from its nationals under the Dollar Securities Mobilization Scheme. Other credits were raised in America, including a British banking credit, bearing 5% interest, for $50,000,000, which matured in June 1917; a credit of $25,000,000 for wheat purchases, which was paid off in 1917; and Treasury Bills for three months which were issued up to a maximum amount of $150,000,000 by Messrs. J. P. Morgan & Co., acting as agents for the British Treasury. Prior to the entry of the United States into the war on April 7 1917, Great Britain raised loans in America totalling $1,131,400,000. After that date the United States Government lent money freely to the British Government direct. An arrangement was made in 1919 by which interest payments on the Government loans were deferred for three years, namely, until 1922, and at the close of the year 1920 the total advances amounted to $4,196,818,000. Loans were raised in Argentina, Uruguay, Spain, Holland, Switzerland, Japan, Chile, and Sweden. The bulk of these were rapidly repaid, but the great bulk of Britain’s debt to America still remained untouched in June 1921.

In two years from April i 1919 the British external debt was reduced by ₤203,000,000; in the financial year ended March 31 1921 the reduction was ₤117,000,000. On that date the total was ₤1,161,560,000 at par of exchange. In the year 1920-21 the British debt to America was reduced by nearly ₤75,000,000, and the debt to Canada by ₤20,000,000. On March 31 1921 the only debt owed to foreign nations apart from the United States was ₤826,000 to Sweden. On the same date the British debt to Canada was $125,000,000.

The 5 % War Loan issued at the beginning of 1917 had become the premier domestic British security, the old consols being now of an inconsiderable amount comparatively and relegated to the background in the market. Cash subscriptions to the loan had amounted to ₤966,048,000, and conversions (of the earlier 412% Loan and Exchequer Bonds) amounted to ₤1,103,797,000, making a total of ₤2,069,845,000.

In December 1915 the principle of “continuous borrowing” was adopted for British Government war-borrowing. On the 17th of that month 5% Exchequer Bonds were put on sale, and realized, in the period which terminated on June 1 1916, ₤237,829,469. Four series of these bonds, the last series bearing 6% interest, were put on sale down to Dec. 30 1916, when the sales were temporarily suspended in preparation for the issue of the 5% War Loan, the greatest loan operation of the war. On April 13 1917 the daily sales of Exchequer Bonds were resumed, 5% Bonds being again offered at par. Sales of Exchequer Bonds, however, were brought definitely to an end on Sept. 22 1917 (partly because, by Statute, this form of issue was limited to a six-year term), and on Oct. 1 1917 a new type of security called National War Bonds, of a character more appropriate for the Government’s requirements, was offered for day-by-day subscription, bearing 5% interest and redeemable at a premium varying from ₤2 to ₤5%, according to the maturity of the bonds, which ranged from 5 to 10 years. A great deal of energy was imparted to the campaign for selling these bonds, and it achieved marked success. Down to March 31 1918 sales of these bonds amounted to no less than ₤616,193,692. The second series, sold between April 1 1918 and Sept. 30 1918, produced ₤483,224,088; the third, between Oct. 1 1918 and Jan. 18 1919, yielded ₤494,399,505; and the fourth, between Feb. 1 1919 and May 31 1919, ₤75,745,151. “Continuous borrowing” amply justified all that was expected of it. By withdrawing from active circulation large amounts of currency the daily borrowing had the effect of holding commodity prices in check, the tendency of the latter being strongly upward on account of the continuous inflation of currency and credit involved by unceasing Government borrowing from the banks. During the war period investors showed a marked preference for short-dated securities, and the Government accordingly offered securities redeemable within a comparatively few years. But with the cessation of hostilities and diminution of expenditure the Government decided to make an attempt to issue a fairly long-term loan with the object of reducing the floating debt, which was then in the neighbourhood of 1,000 millions. On June 12 1919 it issued the first Funding Loan, bearing 4% interest and redeemable at the earliest in 1960, and at the latest in 1990. The bonds were offered at 80% and produced only <references>

- ↑ The high figure for Switzerland is mainly due to the fact that big loans were incurred by the Federal Government for railways.

{kind=link}