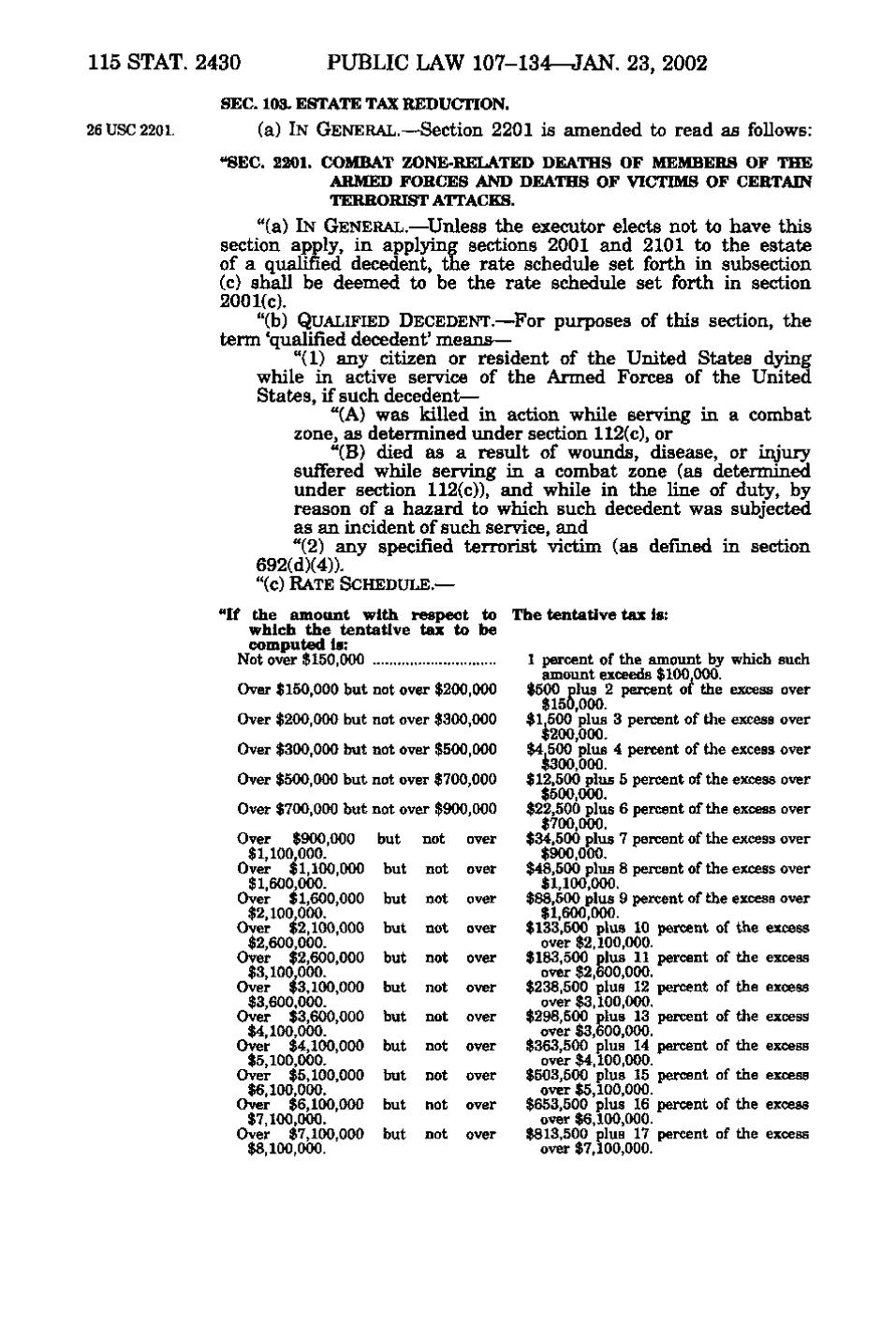

115 STAT. 2430 PUBLIC LAW 107-134-^AN. 23, 2002 SEC. 103. ESTATE TAX REDUCTION. 26 USC 2201. (a) IN GENERAL.—Section 2201 is amended to read as follows: "SEC. 2201. COMBAT ZONE-RELATED DEATHS OF MEMBERS OF THE ARMED FORCES AND DEATHS OF VICTIMS OF CERTAIN TERRORIST ATTACKS. "(a) IN GENERAL,—Unless the executor elects not to have this section apply, in applying sections 2001 and 2101 to the estate of a qualified decedent, the rate schedule set forth in subsection (c) shall be deemed to be the rate schedule set forth in section 2001(c). "(b) QUALIFIED DECEDENT. — For purposes of this section, the term 'qualified decedent' means— "(1) any citizen or resident of the United States dying while in active service of the Armed Forces of the United States, if such decedent— "(A) was killed in action while serving in a combat zone, as determined under section 112(c), or "(B) died as a result of wounds, disease, or injury suffered while serving in a combat zone (as determined under section 112(c)), and while in the line of duty, by reason of a hazard to which such decedent was subjected as an incident of such service, and "(2) any specified terrorist victim (as defined in section 692(d)(4)). "(c) RATE SCHEDULE.— "If the amount with respect to which the tentative tax to be computed is: Not over $150,000 Over $150,000 but not over $200,000 Over $200,000 but not over $300,000 Over $300,000 but not over $500,000 Over $500,000 but not over $700,000 Over $700,000 but not over $900,000 Over $900,000 but not over $1,100,000. Over $1,100,000 but not over $1,600,000. Over $1,600,000 but not over $2,100,000. Over $2,100,000 but not over $2,600,000. Over $2,600,000 but not over $3,100,000. Over $3,100,000 but not over $3,600,000. Over $3,600,000 but not over $4,100,000. Over $4,100,000 but not over $5,100,000. Over $5,100,000 but not over $6,100,000. Over $6,100,000 but not over $7,100,000. Over $7,100,000 but not over $8,100,000. The tentative tax is: 1 percent of the amount by which such amount exceeds $100,000. $500 plus 2 percent of the excess over $150,000. $1,500 plus 3 percent of the excess over $200,000. $4,500 plus 4 percent of the excess over $300,000. $12,500 plus 5 percent of the excess over $500,000. $22,500 plus 6 percent of the excess over $700,000. $34,500 plus 7 percent of the excess over $900,000. $48,500 plus 8 percent of the excess over $1,100,000. $88,500 plus 9 percent of the excess over $1,600,000. $133,500 plus 10 percent of the excess over $2,100,000. $183,500 plus 11 percent of the excess over $2,600,000. $238,500 plus 12 percent of the excess over $3,100,000. $298,500 plus 13 percent of the excess over $3,600,000. $363,500 plus 14 percent of the excess over $4,100,000. $503,500 plus 15 percent of the excess over $5,100,000. $653,500 plus 16 percent of the excess over $6,100,000. $813,500 plus 17 percent of the excess over $7,100,000.

�