120 STAT. 1598

PUBLIC LAW 109–304—OCT. 6, 2006

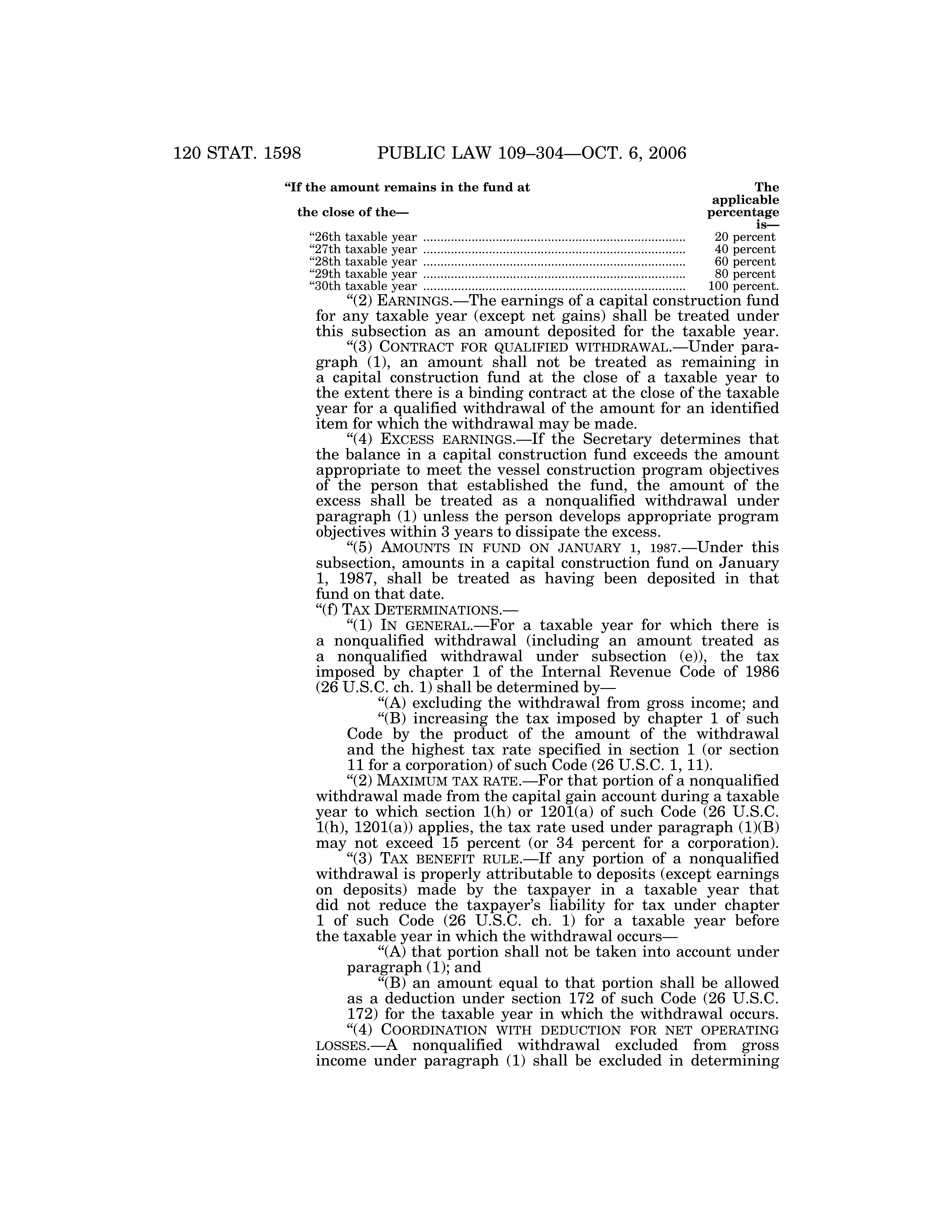

‘‘If the amount remains in the fund at

The applicable percentage is— 20 percent 40 percent 60 percent 80 percent 100 percent.

the close of the— ‘‘26th ‘‘27th ‘‘28th ‘‘29th ‘‘30th

taxable taxable taxable taxable taxable

year ............................................................................ year ............................................................................ year ............................................................................ year ............................................................................ year ............................................................................ EARNINGS.—The earnings of a capital construction

‘‘(2) fund for any taxable year (except net gains) shall be treated under this subsection as an amount deposited for the taxable year. ‘‘(3) CONTRACT FOR QUALIFIED WITHDRAWAL.—Under paragraph (1), an amount shall not be treated as remaining in a capital construction fund at the close of a taxable year to the extent there is a binding contract at the close of the taxable year for a qualified withdrawal of the amount for an identified item for which the withdrawal may be made. ‘‘(4) EXCESS EARNINGS.—If the Secretary determines that the balance in a capital construction fund exceeds the amount appropriate to meet the vessel construction program objectives of the person that established the fund, the amount of the excess shall be treated as a nonqualified withdrawal under paragraph (1) unless the person develops appropriate program objectives within 3 years to dissipate the excess. ‘‘(5) AMOUNTS IN FUND ON JANUARY 1, 1987.—Under this subsection, amounts in a capital construction fund on January 1, 1987, shall be treated as having been deposited in that fund on that date. ‘‘(f) TAX DETERMINATIONS.— ‘‘(1) IN GENERAL.—For a taxable year for which there is a nonqualified withdrawal (including an amount treated as a nonqualified withdrawal under subsection (e)), the tax imposed by chapter 1 of the Internal Revenue Code of 1986 (26 U.S.C. ch. 1) shall be determined by— ‘‘(A) excluding the withdrawal from gross income; and ‘‘(B) increasing the tax imposed by chapter 1 of such Code by the product of the amount of the withdrawal and the highest tax rate specified in section 1 (or section 11 for a corporation) of such Code (26 U.S.C. 1, 11). ‘‘(2) MAXIMUM TAX RATE.—For that portion of a nonqualified withdrawal made from the capital gain account during a taxable year to which section 1(h) or 1201(a) of such Code (26 U.S.C. 1(h), 1201(a)) applies, the tax rate used under paragraph (1)(B) may not exceed 15 percent (or 34 percent for a corporation). ‘‘(3) TAX BENEFIT RULE.—If any portion of a nonqualified withdrawal is properly attributable to deposits (except earnings on deposits) made by the taxpayer in a taxable year that did not reduce the taxpayer’s liability for tax under chapter 1 of such Code (26 U.S.C. ch. 1) for a taxable year before the taxable year in which the withdrawal occurs— ‘‘(A) that portion shall not be taken into account under paragraph (1); and ‘‘(B) an amount equal to that portion shall be allowed as a deduction under section 172 of such Code (26 U.S.C. 172) for the taxable year in which the withdrawal occurs. ‘‘(4) COORDINATION WITH DEDUCTION FOR NET OPERATING LOSSES.—A nonqualified withdrawal excluded from gross income under paragraph (1) shall be excluded in determining

VerDate 14-DEC-2004

13:05 Jul 12, 2007

Jkt 059194

PO 00002

Frm 00342

Fmt 6580

Sfmt 6581

E:\PUBLAW\PUBL002.109

APPS06

PsN: PUBL002

�

{kind=link}