it would be after some have matured. The actual value of any

one risk borne by a company is indeterminate. It may become

a claim to-morrow, or not for a generation to come. In the

former case the company must now hold funds to pay in full;

in the latter, the future premiums will perhaps more than suffice,

so that no present reserve is needed. An entire reserve for the

whole body of risks is essential, and its amount is definite,

upon the reasonable assumption that the general average remains

undisturbed by individual changes. A distinct reserve

for a single policy is inconceivable. To recognize it is to deny the

first principle of insurance. The average amount by which the

reserve of a company must be increased, because of the existence

of policies of a given class, is to the actuary an important fact,

and is commonly accepted as his best guide in the distribution

of surplus. But a popular theory has seized upon the assignment

of this average sum to each policy, in the technical shorthand

of the actuary, and holds that it is in each case the special

property of the owner of that policy. The practical consequences

are serious when, as often, many of the insured cease to pay

premiums, and each demands the amount of the supposed

individual reserve. His right to claim it is countenanced by

a widespread public opinion, which has inspired statutes in

Massachusetts and some other states, requiring companies to

redeem all policies lapsing after the first two or three years of

insurance at a price founded on the technical reserve. Yet, in

by far the majority of instances, the lapse of policies is of itself

a loss to the company. It is deprived of business secured at

much expense before it has derived any of the advantage expected

from the accession. It is compelled to pay numbers of its profitable

contributors for ceasing to contribute. The burden falls in

a mutual company upon the insured who fulfil their contracts.

Such laws favour those who withdraw after few payments at

the cost of those who maintain their insurance to the end, or for

many years. The American companies formerly yielded to the

pressure of a mistaken public sentiment, and competed for

favour by promising excessive values in case of surrender.[1]

Similar conditions exist in Switzerland, Austria, and other

countries in which the business is minutely regulated by government

bureaus. But in Great Britain the companies are largely

free from such influences, while an open market exists for policies

which have a commercial value, with results on the whole more

satisfactory to all parties interested than any rule of compulsory

purchase which could be enforced on the companies.

A special form of life insurance, which has wonderfully developed, is the family insurance of the labouring people by the so-called industrial companies. Until recently this class of people had no satisfactory share in the benefits of insurance, although the friendly societies in Great Industrial Insurance. Britain, and many forms of beneficial associations in the United States, were attempts, often in part successful, to provide for special wants, mainly for maintenance of the sick and for the costs of burial. Most of them, however, lacked a scientific basis and an efficient and permanent organization, while thousands of them were grossly mismanaged. In Germany an elaborate scheme of compulsory insurance for labourers was established by a law of the empire in 1883, and extended in subsequent years; and similar legislation has been enacted in several other countries, most thoroughly in Switzerland and Austria. The ultimate value of this great social experiment cannot yet be determined. That it relieves much want and does a great service in preventing pauperism is not disputed; but that it also undermines the independent spirit of the people, and that it imposes a burden upon the national industry, which not only hampers it in the world’s competition, but reacts with special injury upon the class it aims to benefit, are criticisms not satisfactorily answered. No scheme of government insurance, certainly, is adapted to a people impatient of paternalism in its rulers and thoroughly habituated to voluntary association for all common interests. The solution of the great problem, how to apply the insurance principle to the most pressing needs for protection of the class supported by the wages of labour, is now sought in Great Britain and America mainly in the universal offer to them of industrial insurance. The Prudential Assurance Company of London was the pioneer in this work, beginning it experimentally in 1848, but gradually adapting its methods to the new field, until a generation later they showed themselves so efficient that an extraordinary growth resulted, and has continued without interruption. This company and others upon a similar plan insure whole households together for burial expenses in case of death, and a small provision for dependants or for old age, charging as premiums small fractions of a day’s wages, which must be collected weekly. The great difficulties encountered were the cost of small and frequent collections, and the high rate of mortality, which is from 40 to 90% more than that in the experience of the older companies. This high death-rate is due not so much to the fact that life is shorter in the labouring class as to the lack of efficient medical selection, which would be too costly. The premiums, at best, must be made higher than in offices insuring for annual payments, but the demand for insurance extended as rapidly as the system could be explained, and the Prudential is said to have now in force some 12,000,000 policies, with an average premium of twopence a week, secured by an accumulated insurance fund of £17,000,000. It has superseded a host of petty assessment societies of various classes without scientific basis or business responsibility, which deluded and disappointed the poor. The British government in 1864 undertook to administer a plan for the insurance of working men, but in thirty years accomplished less than the work of one private company in a year. In addition to the many insurance companies which transact industrial business in the United Kingdom, a large number of friendly societies have adopted similar plans.

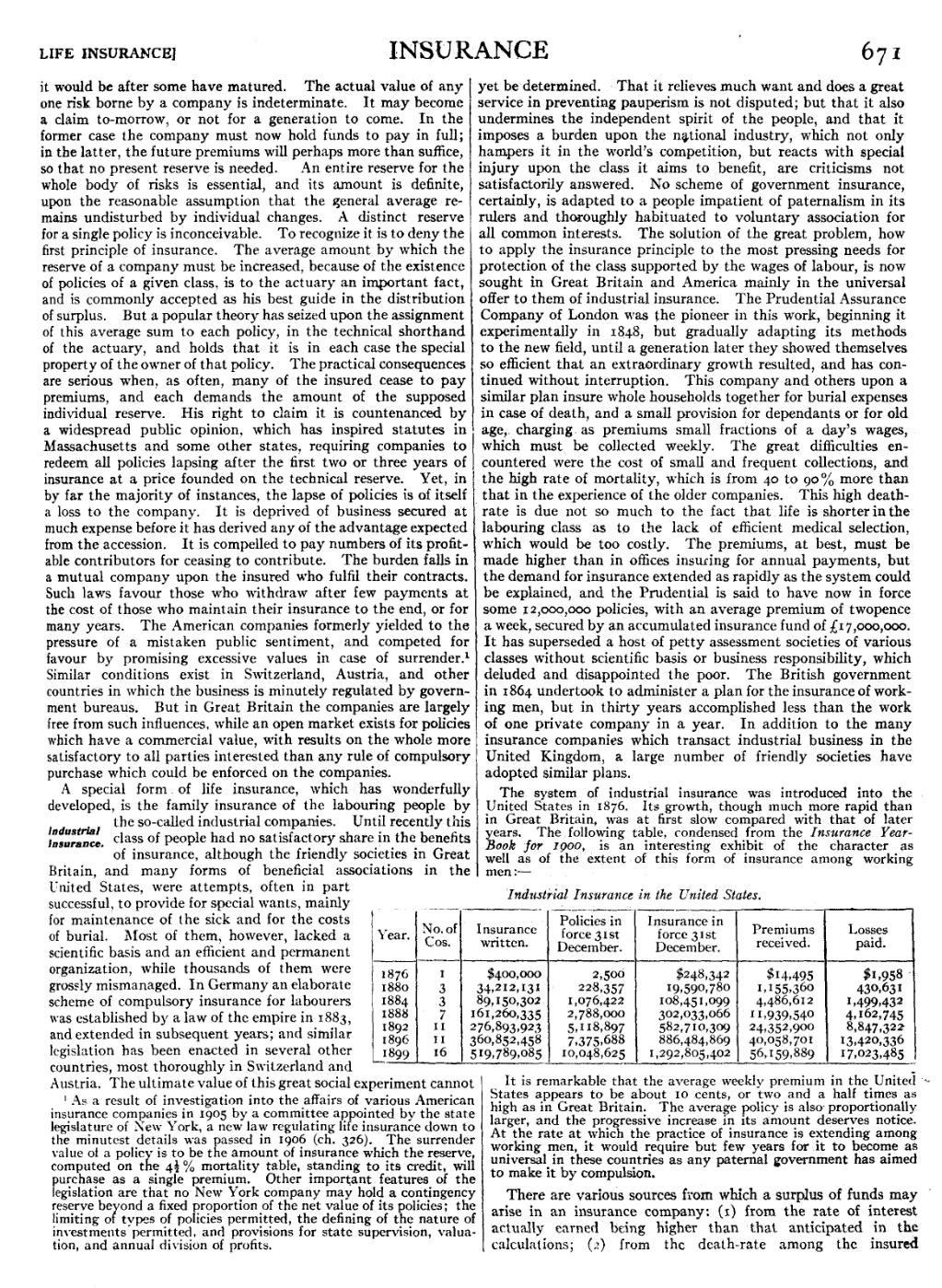

The system of industrial insurance was introduced into the United States in 1876. Its growth, though much more rapid than in Great Britain, was at first slow compared with that of later years. The following table, condensed from the Insurance Year-Book for 1900, is an interesting exhibit of the character as well as of the extent of this form of insurance among working men:—

Industrial Insurance in the United States.

| Year. | No. of Cos. | Insurance written. | Policies in force 31st December. | Insurance in force 31st December. | Premiums received. | Losses paid. |

| 1876 | 1 | $400,000 | 2,500 | $248,342 | $14,495 | $1,958 |

| 1880 | 3 | 34,212,131 | 228,357 | 19,590,780 | 1,155,360 | 430,631 |

| 1884 | 3 | 89,150,302 | 1,076,422 | 108,451,099 | 4,486,612 | 1,499,432 |

| 1888 | 7 | 161,260,335 | 2,788,000 | 302,033,066 | 11,939,540 | 4,162,745 |

| 1892 | 11 | 276,893,923 | 5,118,897 | 582,710,309 | 24,352,900 | 8,847,322 |

| 1896 | 11 | 360,852,458 | 7,375,688 | 886,484,869 | 40,058,701 | 13,420,336 |

| 1899 | 16 | 519,789,085 | 10,048,625 | 1,292,805,402 | 56,159,889 | 17,023,485 |

It is remarkable that the average weekly premium in the United States appears to be about 10 cents, or two and a half times as high as in Great Britain. The average policy is also proportionally larger, and the progressive increase in its amount deserves notice. At the rate at which the practice of insurance is extending among working men, it would require but few years for it to become as universal in these countries as any paternal government has aimed to make it by compulsion.

There are various sources from which a surplus of funds may arise in an insurance company: (1) from the rate of interest actually earned being higher than that anticipated in the calculations; (2) from the death-rate among the insured

- ↑ As a result of investigation into the affairs of various American insurance companies in 1905 by a committee appointed by the state legislature of New York, a new law regulating life insurance down to the minutest details was passed in 1906 (ch. 326). The surrender value of a policy is to be the amount of insurance which the reserve, computed on the 412% mortality table, standing to its credit, will purchase as a single premium. Other important features of the legislation are that no New York company may hold a contingency reserve beyond a fixed proportion of the net value of its policies; the limiting of types of policies permitted, the defining of the nature of investments permitted, and provisions for state supervision, valuation, and annual division of profits.

{kind=link}